What is Tax Diversification

Within the context of public finance, a government that is tax-diversified is one that levies a wide array of tax types. Tax diversification is a policy goal of many governments, as a lack of diversification may disproportionately burden certain groups of taxpayers or expose a government to economic shocks.

Facts versus Headlines

Governments, particularly state governments, are far more diversified than headline statistics suggest. Take New Hampshire, which has neither a sales tax nor a personal earned income tax. Is New Hampshire undiversified? The state government’s largest source of revenue is fees collected and revenue earned from governmental and business-type activities. These fees and revenue comprise 35% of total revenue, surpassing total tax revenue, which makes up only 27% of total revenue.

Now consider Florida, Texas, and South Dakota, three states with no personal income tax. Each state’s sales taxes comprise more than 80% of total tax revenue. When viewed alone, this might suggest that these states are undiversified, but in fact, tax revenue comprises less than one-third of their total revenue, like New Hampshire. All US state governments have not only a mixture of tax types but also a blend of additional revenue from business-type and component unit activities, as well as grants and transfers from federal and local governments.

Local governments are also more diversified than headline statistics suggest. Even a local government whose only source of tax revenue is property tax will collect fees and earn revenue from business-type and component unit activities, and may also receive transfers from the state, all of which are revenue diversifiers.

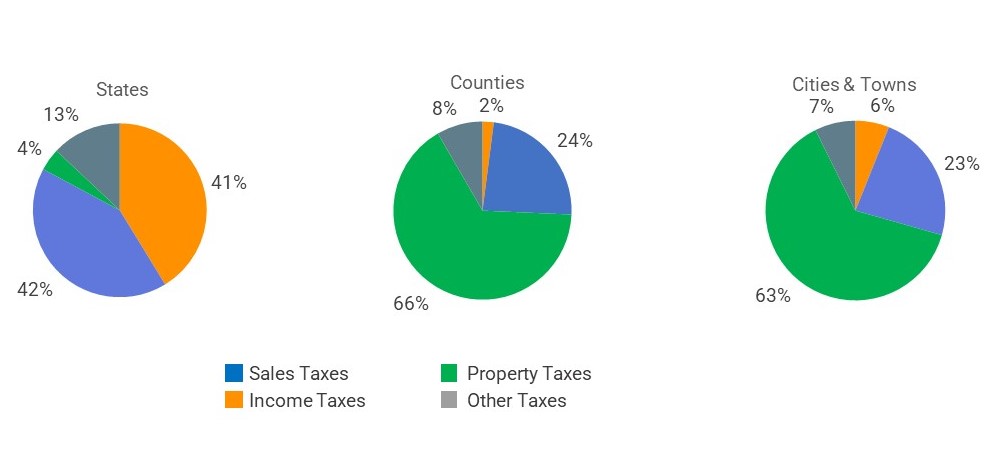

Tax Revenue Diversification

On average, a state’s income and sales taxes constitute 83% of total tax revenue. In counties, 66% of tax revenue comes from property taxes, 24% comes from sales taxes, 8% comes from other taxes, and income taxes contribute 2% to tax revenue. In cities and towns, 63% of tax revenue comes from property taxes, nearly 23% comes from sales taxes, and the remainder comes from income taxes and other taxes at 6% and 7%, respectively.

Source: Pality

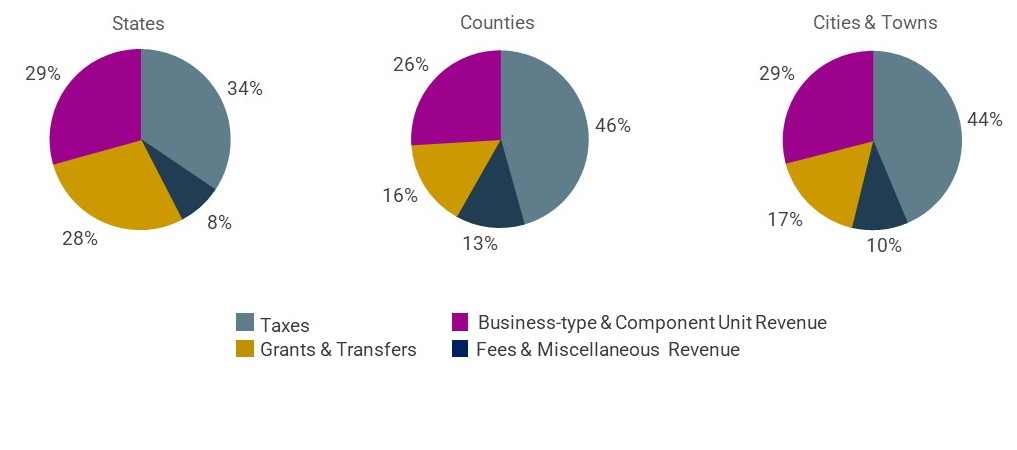

Revenue Diversification

While each jurisdiction type has one or two predominant tax types, for all jurisdiction types, tax revenue comprises less than half of total revenue. In a typical state, tax revenue makes up 34% of total revenue. In a typical county, tax revenue comprises 46% of total revenue, and in a city or town, it makes up 44% of total revenue.

State governments, on average, earn a variety of fees and revenue from business-type and component unit activities. Together, these sources comprise 37% of total revenue, which is greater than the revenue that taxes contribute to total revenue. Transfers and grants, net of outflows to and inflows from cities, counties, and the federal government, make up the balance of about 28% of total revenue.

County governments earn a variety of fees and revenue from business-type and component unit activities as well, which together comprise 39% of total revenue on average. Transfers and grants, net of outflows and inflows, amount to 16% of total revenue.

The average revenue composition in cities and towns is like the revenue composition in counties, with a variety of government fees and revenue from business-type and component unit activities comprising 39% of total revenue and net transfers and grants comprising 17%.

Source: Pality

Tax Diversification for the Taxpayer

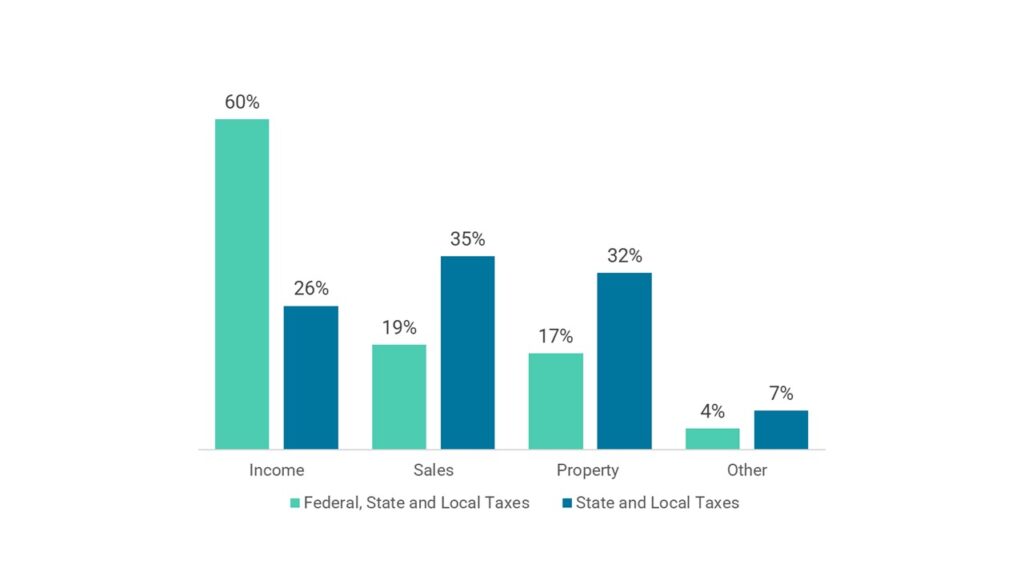

Even if a state or local government’s tax revenue composition is not well-diversified, a taxpayer’s tax burden is well-diversified when viewed in the aggregate. Excluding federal government taxes, the composition of the combined state and local tax burden on taxpayers is quite balanced on average, with sales taxes comprising 35%, property taxes comprising 32%, income taxes comprising 26%, and other taxes comprising 7% of total taxes paid.

If federal taxes are considered, income taxes play an even bigger role. Income taxes comprise 60% of all taxes collected by federal, state, and local governments, excluding payroll taxes. Combined across all jurisdictions, sales taxes comprise 19% of total tax revenue, property taxes comprise 17%, and other taxes account for 4%.

Share of Total Tax Revenue by Type of Tax

Source: Pality

Discussions surrounding tax diversification should address total revenue in addition to tax revenue and focus on diversifying the Tax & Fee Burden on taxpayers.

Written by James Galasso.

Copyright 2023 Pality.

{kind=link}

{kind=link}